A cheque is meant to feel reassuring. It is old-fashioned money, certainly, but still money: formal, legible, faintly ceremonial. It arrives with the authority of paper and ink, the state or the company or the solicitor telling you, in effect, that the sum is real and that it is yours. What it should not become is an expedition.

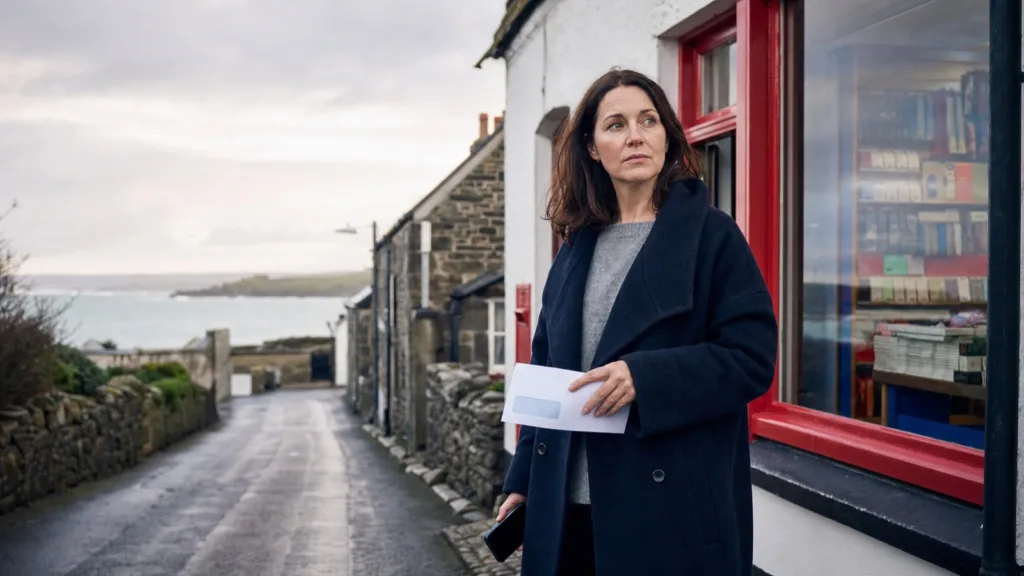

Yet that is precisely what happened in the Annabel Yates Lloyds cheque deposit row, a story that has cut through because it captures something larger than a single customer’s frustration. According to BBC reporting published on 14 May 2026, Annabel Yates of Crackington Haven, Cornwall, received a £900 cheque from HMRC and tried to pay it into her Lloyds account. The app would not scan it. Her local Post Office, she was told, could no longer accept cheque deposits for Lloyds Banking Group customers after a service change introduced in January. In the end, a routine tax refund turned into a 94-mile round trip to Truro.

This is the sort of story banks tend to file under “exception”. The difficulty is that modern life increasingly seems to be built from exceptions. Everything is efficient, seamless and app-enabled until one small thing refuses to behave. Then the whole structure reveals how little resilience has been left in the system.

Why the Annabel Yates Lloyds cheque deposit story has struck a nerve

The annabel yates lloyds cheque deposit story has gathered attention not because people are sentimental about cheques, but because it dramatises a simple fear: that a basic financial task can now collapse if the first digital route does not work. That matters in any part of Britain. In rural Britain, it matters more. Distance turns inconvenience into cost.

Lloyds is entitled to point out that cheque usage has been in long decline. That is true, and the bank has done exactly that. It is also true that Lloyds still offers customers several ways to pay in a cheque: via the mobile app, at a branch, or by post, including Freepost. On paper, that reads like choice. In practice, it reads more like contingency.

The app works until it doesn’t

The app works, unless it does not. The branch works, unless the branch is nowhere near you. The post works, unless you are understandably wary of sending a meaningful sum through the mail and then waiting for the banking system to reassure you that it has arrived safely. A system should not be judged only by the elegance of its preferred route. It should be judged by the dignity of its fallback options.

A cheque is old-fashioned, but not obsolete

There is a temptation, when discussing this kind of case, to frame it as a culture-war skirmish between analogue and digital Britain. That is too lazy. The more revealing point is that even highly digitised systems still depend on awkward leftovers. HMRC’s own current guidance makes clear that tax refunds do not all move in one uniform, frictionless stream. Some customers can claim via bank transfer. Some can request a cheque. Some are told by letter that a cheque will be issued automatically. In other words, the cheque is not a quaint relic accidentally floating around in 2026. It remains part of the machinery.

And if the state still uses the cheque, banks cannot behave as though the cheque is essentially the customer’s private eccentricity.

Where Lloyds’ own guidance becomes part of the problem

That is where this case becomes more interesting than a single consumer gripe. The public guidance itself is not as clean as it ought to be. As checked on 15 May 2026, Lloyds’ guide on how to pay money into your account still says customers can pay in cheques at a Post Office with the correct envelope and a pre-printed paying-in slip. Meanwhile, the bank’s Post Office services page for personal customers now lists cash deposits, withdrawals and balance checks, while steering cheque users back towards the app. The problem is not simply that services change. It is that people are expected to navigate those changes without ambiguity, and the ambiguity is written into the institution’s own public pages.

The Post Office question is where confusion starts

For most readers, this is the practical hinge of the story. If a bank has moved away from one deposit route, the wording around that change has to be brutally clear. The customer should not need to compare help pages like a solicitor reading footnotes.

A banking hub is not always the answer it appears to be

The rural dimension only sharpens the point. Reports around the case included comments from Marshgate postmistress Joanna Bickersteth, who said customers had been frustrated by the removal of cheque deposit services at the Post Office since January. Even more tellingly, a banking hub in Bude was said to be unable to take cheque deposits because that function was tied to Post Office processing rather than the mere existence of a shared banking counter. This is modern Britain in miniature: the infrastructure appears to exist, the signage implies a solution, and then the one thing you actually need turns out to be unavailable.

Why the Lloyds bank row resonates beyond Cornwall

That is why the annabel yates lloyds bank row resonates beyond Cornwall. It is a story about residual dependence. Institutions phase out older habits on the assumption that most people no longer require them, which is perfectly sensible up to a point. But “most people” is not a human being. The remaining use cases are often the ones that arrive at exactly the wrong moment to become complicated: bereavement, probate, tax refunds, reimbursements, insurance claims, one-off payments that are too important to be casual and too infrequent to be well rehearsed.

Rural distance turns inconvenience into cost

An app failure in a city is irritating. An app failure in North Cornwall can become a day. That means petrol, time away from work, childcare rearranged, a bus timetable studied, and the general low-grade exhaustion that institutions rarely count because it does not appear on a balance sheet.

Convenience has become a tone as much as a service

There is also, quietly, a matter of tone. British retail banking now loves the language of convenience. Everything is framed as intuitive, instant, smoother than ever. But convenience that survives only in best-case conditions is not convenience. It is optimism disguised as infrastructure. “Use the app” is not a meaningful solution if the app has already failed. “Post the cheque” is not a neutral suggestion if the customer is worried, with good reason, about risk, delay or simple peace of mind. Convenience, if it is to deserve the name, must take account of trust.

None of this means Lloyds is uniquely villainous. The bank is operating within the same broad logic as the rest of the sector: fewer branches, more digital nudging, more emphasis on customer self-service, more pressure to treat paper as a dwindling edge case. Nor is the wider regulatory picture a complete answer. The FCA’s access-to-cash regime, which came into force on 18 September 2024, is designed to protect reasonable local access to cash withdrawal and deposit services. Important, yes. But it does not magically rebuild every piece of ordinary banking life that has been thinned out over the past decade.

What readers should do with a £900 HMRC cheque now

So what would a sensible response look like, both from the bank and from the customer standing in the middle of the problem?

If the Lloyds app rejects the cheque

Start with the app, because Lloyds still presents it as the primary route. But if the scan fails, do not keep repeating the same step in the hope that patience will become a banking channel. Check whether the cheque is less than six months old, make sure the details are clean and legible, and confirm whether the image quality is the problem rather than the cheque itself.

If you need a fallback route

If the app does not work, check branch options before travelling and do not assume your local Post Office or banking hub will handle the deposit. Lloyds also says cheques can be paid in by post, including through Freepost, but that will not suit every customer equally. A route may be technically available and still feel like an unsatisfactory answer.

If the cheque came from HMRC

If the payment originated with HMRC, it is worth checking whether a bank transfer route is available for future claims, because the state’s own systems are now split between digital and paper. That does not solve the cheque already in your hand, but it may spare you the same ritual next time.

First, consistency. If Lloyds no longer wants personal customers to think of the Post Office as a viable route for cheque deposits, that needs to be made plain everywhere, not implied on one page and contradicted on another. Second, candour. If app scanning can fail on certain formats or conditions, say so clearly before the customer reaches the point of irritation. Third, redundancy. If a bank continues to accept cheques, then at least one fallback option should feel local, legible and trusted rather than technically available but emotionally threadbare.

The cheque itself may be a diminishing instrument. The feelings it exposes are not. What unnerves people is not simply the disappearance of branches or the rise of apps; it is the suspicion that the burden of making the system work has quietly been handed back to the customer. You hold a valid payment in your hand. It should not require strategy, interpretation and a day trip.

That is why this story lingers. A £900 HMRC cheque ought to be a dull administrative fact. Instead it has become a neat little parable about British institutions in 2026: streamlined in theory, conditional in practice, and surprised when the public notices the difference.

FAQ

Can Lloyds accept a £900 HMRC cheque?

Yes. Lloyds says personal customers can still pay in cheques through the mobile app, at a branch, or by post.

Why might the Lloyds app refuse to scan a cheque?

Lloyds says some cheque formats are not eligible for app deposit, and image quality can also cause a rejection. If the app fails once, it is better to check the cheque and your fallback options than to keep retrying blindly.

Can you still pay a Lloyds cheque in at the Post Office?

That is where current customer guidance appears inconsistent. One Lloyds help page still references Post Office cheque deposits with the right materials, while the bank’s current Post Office services page focuses on cash services and pushes cheque users back towards the app. It is safest to check before travelling.

Can a banking hub take a cheque deposit for Lloyds?

Not always. Reporting around the Annabel Yates case suggested that even a nearby banking hub in Bude could not handle cheque deposits because that function was tied to Post Office processing.

Can HMRC send a refund by bank transfer instead of cheque?

Sometimes, yes. GOV.UK says some refunds can be claimed online by bank transfer, while other cases still involve HMRC sending a cheque automatically or on request.